The surging use of near-to-eye (NTE) devices is also creating an extensive requirement for microdisplays worldwide. At present, consumer electronic product manufacturers are increasingly manufacturing microdisplays equipped with NTE-device-based applications, such as HUDs, augmented reality (AR)/VR, full-color projection devices, mobile phones, and cameras to meet the high-volume demand for such devices from several end-use industries.

For instance, the media and entertainment and gaming industries are creating a huge demand for NTE-enabled AR/VR devices, whereas, the automotive and military sectors are adopting an enormous volume of HUDs. The product type segment of the microdisplay market is categorized into NTE device, projector, HUD, and others, such as rifle scopes, thermal imaging glasses, and monocular and binocular systems.

Among these, the HUD category is projected to demonstrate the fastest growth during the forecast period, owing to the surging public awareness about vehicle safety and increasing implementation of stringent vehicle safety norms. The convenience offered by the combination of HUD systems and navigation technology is encouraging the adoption of these systems in passenger and commercial vehicles.

These microdisplay products are based on OLED, liquid crystal display (LCD), liquid crystal on silicon (LCOS), or digital light processing (DLP) technologies. In recent years, microdisplay manufacturers, such as Panasonic Corporation, HOLOEYE Photonics AG, Jade Bird Display, US Micro Products Inc., Micledi Microdisplays BV, RAONTECH Co. Ltd., Optovate Ltd., and Shenzhen Anpo Intelligence Technology Co. Ltd., have produced a large quantity of OLED microdisplays, due to their huge requirement in consumer electronics, owing to their compact size, high resolution, and better picture quality.

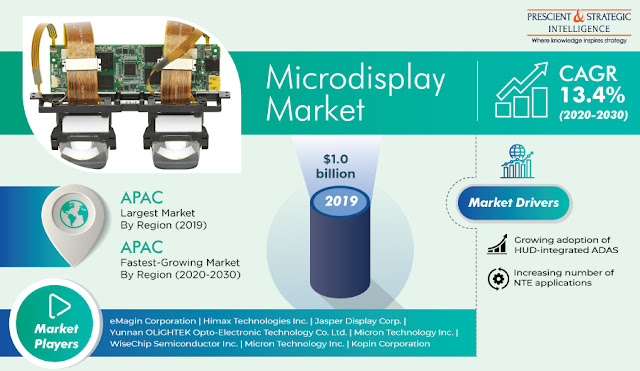

Geographically, Asia-Pacific (APAC) accounted for the largest share in the microdisplay market during the historical period (2014–2019), due to the presence of a considerable number of market players and the availability of microdisplays at affordable prices in the region. Moreover, the existence of flourishing automotive and consumer electronics industries in China and Japan is also driving the demand for microdisplay-based devices in the region.

These microdisplay products are based on OLED, liquid crystal display (LCD), liquid crystal on silicon (LCOS), or digital light processing (DLP) technologies. In recent years, microdisplay manufacturers, such as Panasonic Corporation, HOLOEYE Photonics AG, Jade Bird Display, US Micro Products Inc., Micledi Microdisplays BV, RAONTECH Co. Ltd., Optovate Ltd., and Shenzhen Anpo Intelligence Technology Co. Ltd., have produced a large quantity of OLED microdisplays, due to their huge requirement in consumer electronics, owing to their compact size, high resolution, and better picture quality.

Geographically, Asia-Pacific (APAC) accounted for the largest share in the microdisplay market during the historical period (2014–2019), due to the presence of a considerable number of market players and the availability of microdisplays at affordable prices in the region. Moreover, the existence of flourishing automotive and consumer electronics industries in China and Japan is also driving the demand for microdisplay-based devices in the region.

According to the Organization of International Automobile Manufacturers (OICA), 25,225,242 vehicles and 8,067,557 vehicles were manufactured in China and Japan, respectively, in 2020. Therefore, the surging incorporation of ADAS and HUDs in automobiles and the burgeoning demand for NTE devices will boost the adoption of microdisplays globally.